Duane Morris Takeaway: This week’s episode of the Class Action Weekly Wire features Duane Morris partner Jerry Maatman and associate Nelson Stewart with their discussion of significant developments in the securities fraud class action space, including analysis of two key rulings, class certification rates, and major settlements.

Check out today’s episode and subscribe to our show from your preferred podcast platform: Spotify, Amazon Music, Apple Podcasts, Samsung Podcasts, Podcast Index, Tune In, Listen Notes, iHeartRadio, Deezer, and YouTube.

Episode Transcript

Jerry Maatman: Thank you loyal blog readers for joining us for the next episode of our podcast series, the Class Action Weekly Wire. I’m Jerry Maatman, a partner in Duane Morris’ Chicago and New York offices, and joining me today is my colleague from our New York office, Nelson Stewart. Welcome.

Nelson Stewart: Thank you. Great to be here, Jerry.

Jerry: Today we wanted to discuss trends, issues, and important developments in the area of securities fraud class action litigation. Nelson, this is a big space, but could you give us, from your thought leadership perspective, some kind of summary of what you think are kind of key developments in this area?

Nelson: Sure, Jerry. Class action securities fraud claims typically involve an alleged public misrepresentation or omission made by the issuer of a security, a subsequent disclosure that reveals the statement or omission to be false, and a decrease in the value of the security resulting from the disclosure. Securities fraud claims readily lend themselves to class-wide treatment because the number of investors who may claim losses resulting from a misrepresentation is often considerable.

The principal federal statutes for securities fraud claims are the Securities Act of 1933 and the Securities Exchange Act of 1934. Both statutes were enacted for the purpose of regulating securities markets and providing increased disclosure and transparency for investors in the wake of the stock market crash in 1929.

The 1933 Act generally applies to misrepresentation made in connection with an initial offering of securities. The 1934 Act imposes liability for misrepresentations related to the purchase or sale of existing securities.

Jerry: Thanks, Nelson, for that framework. By my way of thinking, the absolute Holy Grail in class action litigation for the plaintiffs’ bar is class certification. They file the case, they certify it, and then they monetize it. How did plaintiffs fare over the last year in terms of certifying securities fraud class actions?

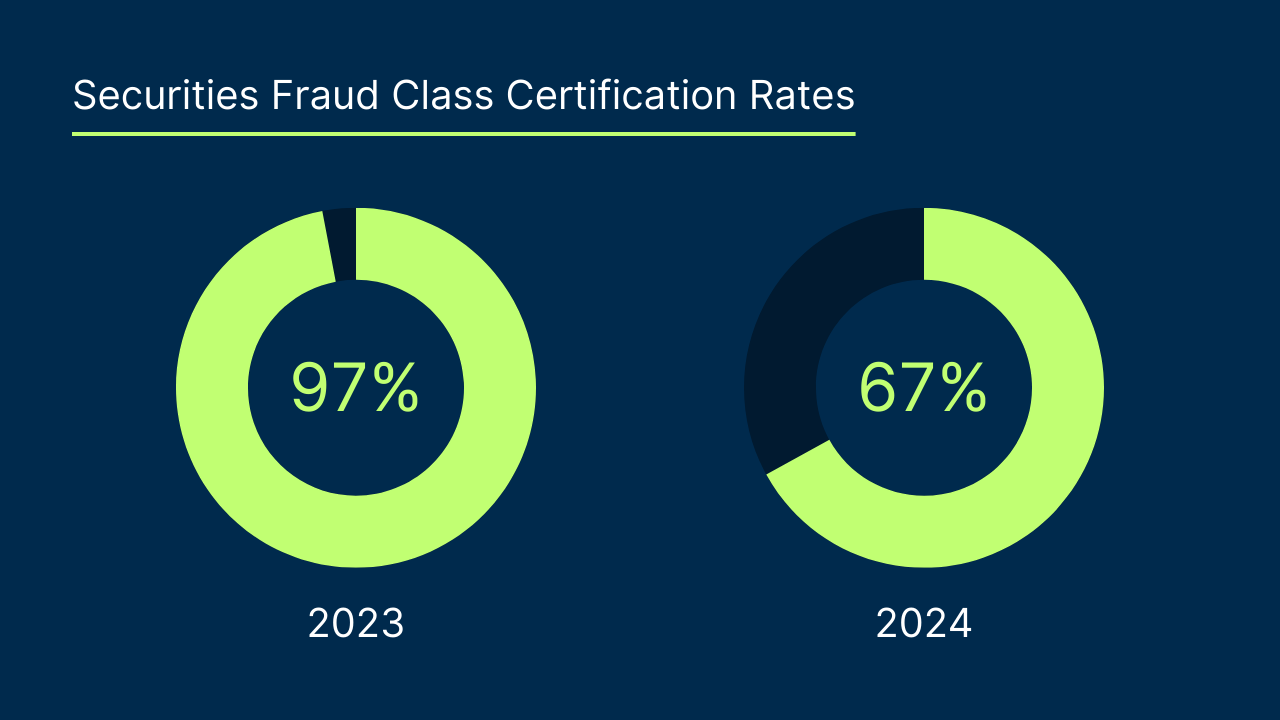

Nelson: In 2023, plaintiffs were incredibly successful in gaining class certification. The plaintiffs’ bar secured class certification at a rate of 97% – or put another way, 35 of 36 motions. Companies secured denials in 3% of the rulings, or just in one case.

Jerry: While we do a comparative study of securities fraud with respect to other areas of law, at least in 2023 securities fraud class certification rates were the highest. We recently did a mid-year report in 2024, and still very high, but down to about 67% – 10 out of 15 cases certified in the securities fraud area. In terms of the key guide posts on the playing field when it comes to securities fraud class action litigation, what are some of the key developments that corporate counsel should be aware of?

Nelson: One of the most notable decisions in 2023 was the U.S. Supreme Court’s ruling in Slack Technologies v. Pirani, et al. The Supreme Court addressed a split among the federal circuits created by the Ninth Circuit’s departure from a well-established interpretation of Section 11(a) of the 1933 Act. A plaintiff bringing a fraud claim under the 1933 Act must show that the purchase of shares at issue can be traced back to the false or misleading registration statement. The statute imposes strict liability and a lower standard of proof for a narrower class of securities than the 1934 Act, which applies to misrepresentations or omissions for any security, but carries a higher standard of that requires plaintiffs to show a scienter, reliance, and loss causation.

In Slack, plaintiffs had purchased shares through a direct listing that offered both registered and unregistered stock shares. The inability to trace unregistered shares to a registration statement would be fatal to plaintiffs’ claims under the 1933 Act. In denying defendant’s motion to dismiss the class action, the district court attempted to accommodate the traceability challenges of a direct listing through a broad reading of the “such security” phrase of Section 11(a). The district court held that the unregistered shares were “of the same nature” as shares subject to the registration statement and plaintiffs therefore had standing under Section 11(a) to bring the suit.

On appeal, the Ninth Circuit noted that the application of Section 11(a) to the direct listing was one of first impression and it affirmed the district court’s decision while rejecting its broader reading of Section 11(a). The Ninth Circuit expressed concern that the more restrictive reading of the statute advocated by Slack, and applied by other circuits, would limit an issuer’s liability for false or misleading statements through the use of a direct listing and thereby disincentivize the 1933 Act’s goal of transparency.

On further appeal, the Supreme Court vacated the Ninth Circuit’s decision and held that the language of the 1933 Act was intended to narrow its focus. Citing Sections 5, 6 and 11(e) as support for the conclusion that the term “such security” refers back to shares that are subject to the registration.

Slack confirms that the novelty of a specific type of offering, such as a direct listing, cannot excuse the well-settled requirements for claims brought under Section 11 of the 1933 Act. Unregistered shares from a direct listing or certain post-IPO offerings are subject to dismissal at the pleading stage for lack of standing under Section 11 if those shares cannot be traced back to the initial registration. Whether an issuer is required to register all shares for sale in a direct listing was not addressed in Slack because this question had not been raised in the prior proceedings.

Another key ruling came out of the Southern District of New York in a case titled Underwood, et al. v. Coinbase Global. There, plaintiffs brought claims under Sections 5 and 12(a) of the 1933 Act and Sections 5 and 29(a) of the 1934 Act. Plaintiffs alleged that Coinbase operated a securities exchange without registering with the SEC. Their amended complaint also alleged that the cryptocurrency tokens sold on the Coinbase platform were securities as defined under both statutes.

However, the issue of whether digital assets must be registered with the SEC was not determined because the court found the plaintiffs failed to state a claim under the 1933 Act and the 1934 Act. Section 5 of the 1933 Act prohibits any person from selling unregistered securities unless the securities are exempt from registration. Section 12(a) creates a private right of action for any buyer against the seller of an unregistered security. To meet the definition of a seller under Section 12(a), a seller must either pass title or other interest directly to the buyer, or the seller must solicit the purchase of a security for its own financial interest. The court granted Coinbase’s motion to dismiss the claims brought under 12(a) because the plaintiffs did not sufficiently plead either requirement.

The initial complaint had stated that there was no privity between a user of the Coinbase platform and Coinbase. The user agreement also expressly stated that Coinbase was simply an agent, and a user who purchased a token from through the online platform was not purchasing digital currency from Coinbase. Though the plaintiffs had attempted to avoid this issue by amending their complaint to state that privity only existed between the user and Coinbase, the court held that it would not allow an amended complaint to supersede the admissions in the plaintiffs’ earlier pleading, or the express language of the user agreement. These facts precluded an action against Coinbase under Section 12(a). The company did not meet the definition of a statutory seller as defined in Section 12(a) because it did not pass title directly to a buyer. The plaintiffs also failed to plead anything more than collateral participation in the purchase of the tokens. The court concluded that absent allegations that the plaintiffs purchased the tokens as a result of active solicitation by Coinbase, Section 12(a) was inapplicable.

The court further held that the plaintiffs’ claims under the 1934 Act also failed for lack of privity. Section 29(a) of the 1934 Act provides that every contract that violates any provision, rule, or regulation is void. The plaintiffs argued that the user agreement and the transactions were void because they involved contracts that were premised on an illegal purchase of an unregistered security on an unregistered exchange, which violated Section 5 of the 1934 Act. The amended complaint sought rescission of the transaction fees and the transactions. To allege a violation of Section 29(b), the plaintiff is required to show that: (i) the contract involved a prohibited transaction; (ii) the plaintiff is in contractual privity with the defendants; and (iii) the plaintiff is in a class that the 1934 Act intended to protect. The court again found that privity was not established under the user agreement. The initial complaint asserted that the plaintiffs contracted with users of the Coinbase platform, not Coinbase. Thus there was no contractual privity with Coinbase. The court also noted that the user agreement was not a contract that required the plaintiffs to do anything illegal. A party to the user agreement was free to use the platform to transact crypto currencies or not transact at all. The court concluded this was insufficient to render the sale of digital assets on the platform a prohibited transaction under Section 5 of the 1934 Act.

Recently, in April of 2024, the Second Circuit reversed the district court’s dismissal of alleged Securities Act violations, fin ding the district court improperly relied on the plaintiffs’ initial complaint and Coinbase’s user agreement, instead of looking solely to the allegations in the amended complaint. The Second Circuit noted that some versions of the user agreements in place when the transaction at issue occurred had conflicting language that could plausibly support the allegations that defendants had passed title to the plaintiffs under Section 12(a)(1) of the 1933 Act. The court upheld dismissal of certain claims brought under the Securities and Exchange Act of 1934, finding that the plaintiff’s conclusory out allegations provided insufficient detail to support a claim for rescission.

Jerry: Thanks for that analysis. Evident to see a lot of developments in this space over the past 12 months. In terms of that monetization of securities fraud class actions, how did the plaintiffs’ bar do on the settlement front?

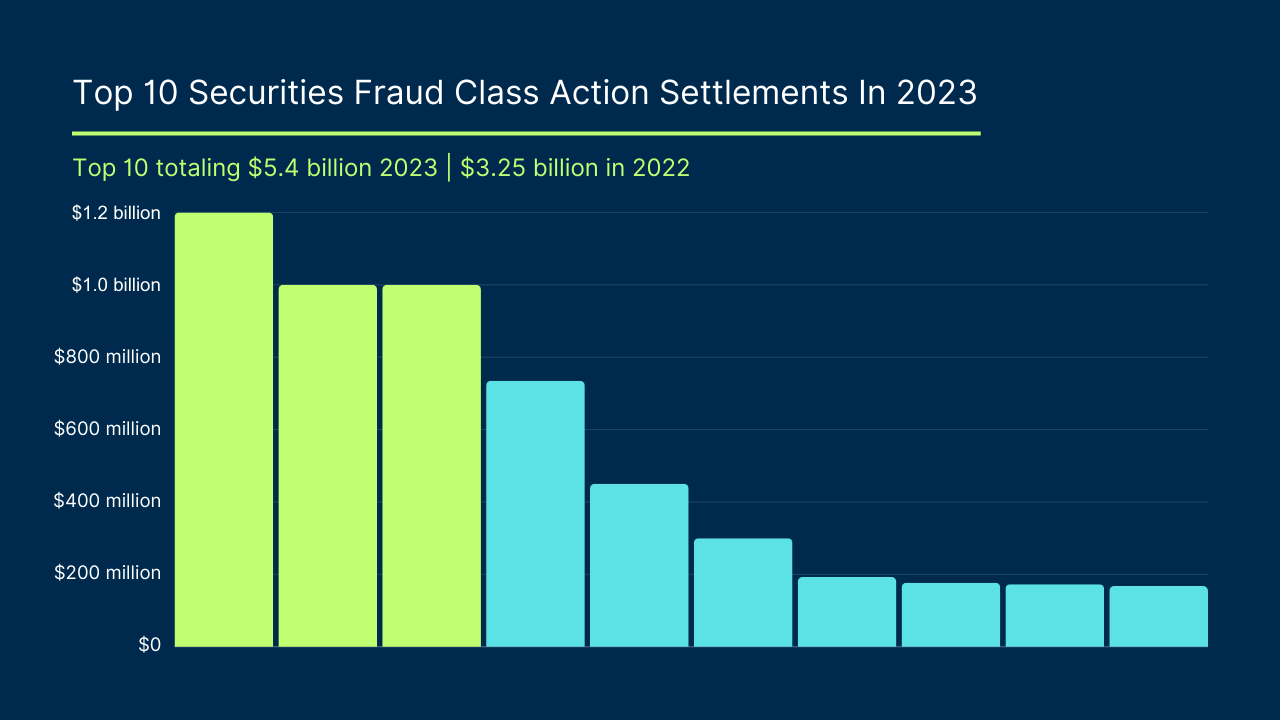

Nelson: There were several settlements of over a billion dollars reached in securities fraud class actions last year, and the top 10 class action settlements in this space add up to $5.4 billion.

In SEC, et al. v. Stanford International Bank, the Court granted approval of a $1.2 billion settlement to resolve investors’ allegations that the banks aided Robert Allen Stanford’s $7 billion Ponzi scheme.

A $1 billion settlement was approved in In Re Dell Technologies Inc. Class V Stockholders Litigation, which was a class action brought by investors alleging Dell, its controlling investors, and its affiliates shortchanged shareholders by billions in a deal that converted Class V stock to common share.

And in In Re Wells Fargo & Co. Securities Litigation, another $1 billion settlement was approved in a class action brought by investors alleging that the company made misleading statements about its compliance with federal consent orders following the 2016 scandal involving the opening of unauthorized customer accounts.

Jerry: It seems like 2024 is equally upbeat for the plaintiffs’ bar. We’ve tracked through the first six months settlements totaling over $2 billion, with three individual settlements near the half-billion mark: $580 million, $490 million, and $434 million for securities fraud class action settlements, so a very robust area for the plaintiffs’ bar.

Well, thanks so much for your insights, Nelson. Very, very helpful in this space. And thank you to our loyal listeners for tuning in to this episode of the Class Action Weekly Wire.

Nelson: Thanks everyone.