Duane Morris Takeaway: This week’s episode features Duane Morris partner Jerry Maatman, senior associate Anna Sheridan, and associate Caitlin Capriotti with their discussion of the key trends and developments analyzed in the 2026 edition of the FCRA Class Action Review.

Check out today’s episode and subscribe to our show from your preferred podcast platform: Spotify, Amazon Music, Apple Podcasts, Podcast Index, Tune In, Listen Notes, iHeartRadio, Deezer, and YouTube.

Episode Transcript

Jerry Maatman: Welcome to our listeners. Thank you for being here for our weekly podcast series, the Class Action Weekly Wire. I’m Jerry Maatman, a partner at Duane Morris, and joining me today on the podcast are my colleagues Anna Sheridan and Caitlin Capriotti. Thanks so much for being with us today.

Anna Sheridan: Thank you, Jerry. I’m happy to be a part of the podcast.

Caitlin Capriotti: Yes, thanks so much for having me, Jerry.

Jerry: Today, we’ll be discussing the second edition of the Duane Morris Fair Credit Reporting Act Class Action Review. Listeners can find this e-book publication and desk reference on our blog, the Duane Morris Class Action Defense Blog. Anna, can you tell our listeners a little bit about the desk reference?

Anna: Yeah, absolutely, Jerry. This review dives deep into the world of consumer protection laws, specifically the Fair Credit Reporting Act (the FCRA), the Fair and Accurate Credit Transactions Act (the FACTA), and the Fair Debt Collection Practices Act (the FDCPA). Since these areas have long been a focus of litigation, particularly for class actions, Duane Morris created this review to analyze the key rulings and developments in these areas in 2025, and the significant legal decisions and trends impacting the type of class action litigations for 2026. We hope that companies will benefit from this resource in their compliance with these evolving laws and standards.

Jerry: Great, let’s start with the basics. The FCRA, as enacted by Congress, aims to ensure that consumer reporting agencies and employers act responsibly and fairly in using background checks and credit checks. Caitlin, can you give us a quick overview of the substantive key provisions of the FCRA?

Caitlin: Yes, of course. The FCRA is focused on ensuring that consumer reporting agencies, or CRAs, maintain accuracy, fairness, and respect for consumers’ privacy rights. It mandates that CRAs follow reasonable procedures to ensure that consumer reports are as accurate as possible. The law also requires employers to disclose when they are obtaining a consumer report on an applicant for a job, and to follow specific procedures if they decide to take adverse action based on that report. Well, FCRA violations often do come down to technicalities, things like failure to provide proper disclosures or obtaining consent incorrectly, and the penalties can be significant, ranging from $100 to $1,000 per violation, with punitive damages up to $2,500 if the violation is deemed willful.

Jerry: Well, thanks so much. Anna, what about the FACTA?

Anna: FACTA requires consuming reporting agencies to present information in a clearer, more understandable manner. One of the key parts of the FACTA is the requirement for adverse action doses. If a consumer is denied credit or offered less favorable terms based on their credit report, they must be informed. This gives consumers the opportunity to dispute any inaccuracies. In fact, it also emphasizes the need for better protections against identity. Similar to the FCRA, the plaintiffs’ bar has been aggressive in bringing class action lawsuits under FACTA, particularly when the accuracy of credit reports and whether consumers are properly notified when adverse actions are taken. The penalties for noncompliance with FACTA are very much in line with the FCRA violation – up to $2,500 for willful violence. However, there have been some significant Supreme Court rulings that have limited the scope of these lawsuits, especially when it comes to proving actual harm or injury-in-fact.

Jerry: Thank you. I’ll go over the last one, which is the FDCPA, the federal Fair Debt Collection Practices Act. This statute governs debt collection practices, and while it doesn’t directly address credit reporting, it’s closely related, because many debt collectors rely on credit reports to pursue collection actions. The FDCPA regulates how they can communicate with individuals. The information that must be disclosed and their conduct during the collection process. In essence, it’s a companion law that protects consumers in the broader context of both credit and debt. So, in terms of these three statutes, what were some of the notable trends that we saw in the class action space in 2025?

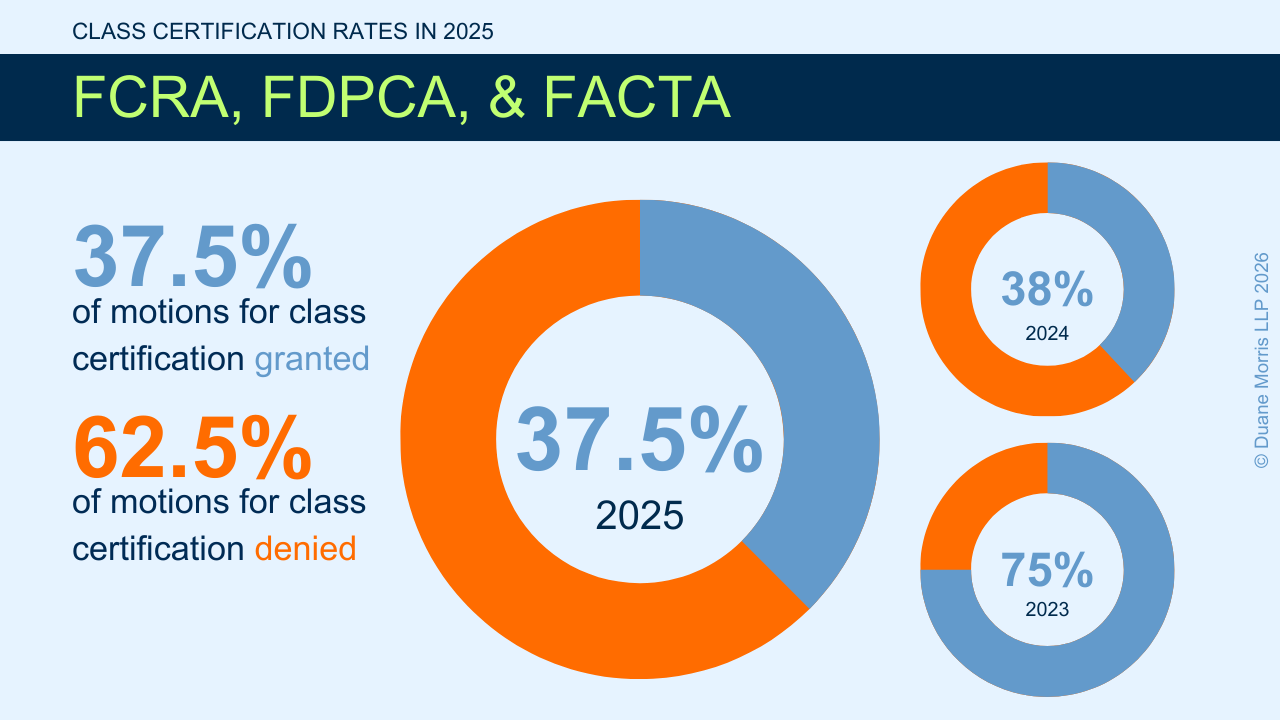

Anna: One notable thing was that courts granted motions for class certification in these cases at almost the exact same rate in 2025 as they did in 2024. Both were around 38%. These rates were down significantly from the 75% of motions being granted in 2023. This could partly be due to the 2021 TransUnion decision and the increasing complexity of FCRA violations. Employers and consumer reporting agencies are now more careful about complying with technical requirements. And plaintiffs are facing higher hurdles in improving harm.

Caitlin: Another thing we’re seeing is the rise of state-level laws that track the FCRA but impose even stricter standards. States like California, New York, and Texas have their own consumer credit reporting laws, and companies need to stay on top of both federal and state regulations to avoid liability.

Jerry: Well, it seems like this area is very much like the rest of the class action state or space where judicial precedents are constantly evolving, and the obligations and duties of companies are in a state of flux. By your way of thinking, what were some of the key, important rulings in this space in 2025?

Caitlin: Yes, so one of the important rulings was Fausett v. Walgreen Co., where the Illinois Supreme Court ruled that plaintiffs bringing claims under the FCRA, or its amendment FACTA, must show a concrete injury to have standing in Illinois state courts. The court held that because the FCRA does not explicitly identify who may sue, plaintiffs cannot rely on statutory standing based solely on a technical violation. Instead, they must meet common law standing, which requires a distinct and concrete injury. In this case, the plaintiff alleged that Walgreens printed too many digits of her debit card number on a receipt, violating FACTA, but she admitted she suffered no actual harm, such as identity theft or misuse of the receipt. The court found this insufficient and ruled that the plaintiff lacked standing overturning the class certification. The decision blocks no-injury FCRA/FACTA lawsuits in Illinois state courts, aligning them more closely with federal standing rules established in Spokeo v. Robins, and potentially affecting other federal statutes with similar private action provisions.

Jerry: That is a key ruling. Certainly, it underscores the M.O. of the plaintiffs’ bar to find a case, file it, certify it, and then monetize it with a settlement. How did the plaintiffs’ bar do in this space in 2025 in terms of class action settlements?

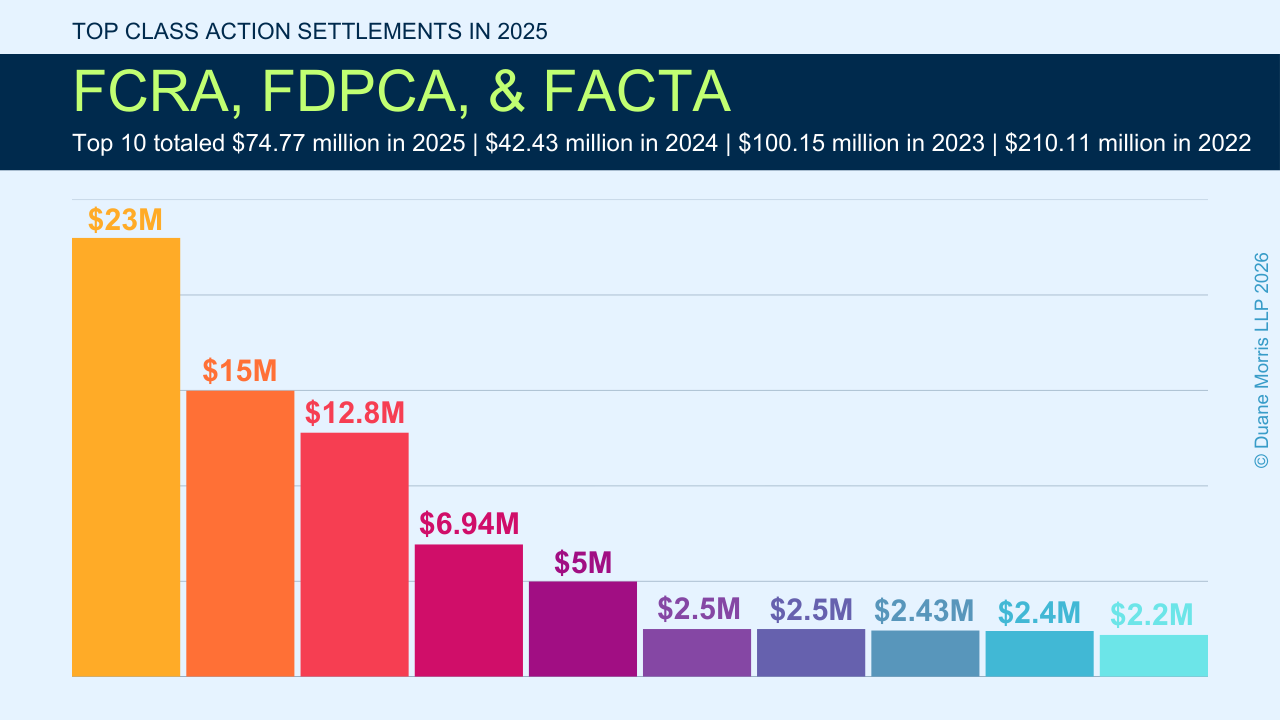

Anna: In 2025, the top 10 FCRA, FDCPA, and FACTA settlements totaled $74.77 million. This was a significant increase from the prior year, when the top 10 class action settlements totaled $42.43 million. However, it’s lower than 2023, when the top 10 settlements totaled just around $100 million.

Jerry: Well, we continue to track class action settlements in all substantive areas on a 24-7, 365 basis, and so we’ll be analyzing and providing analytics on those numbers throughout the year. Thank you both for being here today, and thank you, our loyal listeners, for tuning in. Please stop by our website and our blog for a free copy of the FCRA Class Action Review e-book.

Caitlin: Thank you so much for the opportunity, Jerry.

Anna: Thanks for having me, Jerry, and thanks to everyone for listening.