Duane Morris Takeaway: This week’s episode of the Class Action Weekly Wire features Duane Morris partners Jerry Maatman and Shireen Wetmore and special counsel Shannon Noelle with their discussion of the key trends analyzed in the 2025 edition of the FCRA Class Action Review, including notable Third and Eleventh Circuit rulings shaping related litigation in 2025.

Bookmark or download the FCRA Class Action Review – 2025, which is fully searchable and viewable from any device.

Check out today’s episode and subscribe to our show from your preferred podcast platform: Spotify, Amazon Music, Apple Podcasts, Samsung Podcasts, Podcast Index, Tune In, Listen Notes, iHeartRadio, Deezer, and YouTube.

Episode Transcript

Jerry Maatman: Welcome to our listeners. Thank you for being here for our weekly podcast series, the Class Action Weekly Wire. I’m Jerry Maatman, a partner with Duane Morris, and joining me today are Shireen Wetmore and Shannon Noelle. Thanks so much for being here on our podcast.

Shireen Wetmore: Thanks, Jerry, happy to be part of the podcast.

Shannon Noelle: Thanks for having me, Jerry.

Jerry: Today on the podcast we’re discussing the first-ever publication of the Duane Morris Fair Credit Reporting Act, or FCRA, Class Action Review. Listeners can find our new e-book publication on our blog, the Duane Morris Class Action Defense Blog. Shireen, can you tell our listeners about this new publication and desk reference?

Shireen: Absolutely, Jerry. This Review is brand new, and it dives deep into the world of consumer protection laws. Specifically, the Fair Credit Reporting Act (FCRA), the Fair and Accurate Credit Transactions Act (FACTA or the FACT Act), which amends FCRA, and the Fair Debt Collection Practices Act (FDCPA). A lot of alphabet soup here. These statutes have long been fodder for significant litigation, particularly for class actions. So, Duane Morris created this Review to analyze the key rulings and developments in these areas in 2024 and the significant legal decisions and trends that will be impacting this type of class action litigation for 2025. We hope that companies will benefit from this resource in their compliance with these evolving laws and standards.

Jerry: Great. Let’s start a little bit with the basics. The FCRA, as enacted by Congress, aims to ensure that consumer reporting agencies act responsibly and fairly, but at the same time it’s been an engine for class action litigation. Shannon, can you give us a quick overview of what our listeners need to know about the FCRA?

Shannon: Absolutely. The FCRA is focused on ensuring that consumer reporting agencies, CRAs, maintain accuracy, fairness, and respect for consumers’ privacy rights. It mandates that CRAs follow reasonable procedures to ensure that consumer reports are as accurate as possible. The law also requires employers to disclose when they’re obtaining a consumer report on an applicant for a job and to follow specific procedures if they decide to take adverse action based on the report. FCRA violations often come down to technicalities – things like failure to provide proper disclosures or obtaining consent incorrectly – and the penalties can be significant, ranging from $100 to $1,000 per violation, with punitive damages up to $2,500. If the violation is deemed willful, because of the way the law is structured, it’s relatively easy for plaintiffs to bring class action lawsuits, especially when there are clear procedural missteps that affect many people. Even if actual damages aren’t proven, these technical violations can still lead to successful lawsuits.

Jerry: Thank you. By contrast, Shireen, what about the FACTA? What are the issues in that particular space of litigation?

Shireen: So, the FACTA amended the FCRA, and it was aimed at enhancing consumer protections. It requires consumer reporting agencies, just as Shannon mentioned, to present information in a clear, more understandable manner. And the FACTA really emphasizes the need for better protections against identity theft under the FCRA and the FACT Act. There are significant penalties, nuanced protections that can lead to very large lawsuits with what may seem like only informational injuries. However, there have been some significant Supreme Court rulings over the years that have limited the scope of these lawsuits, and especially when it comes to proving actual harm or injury in fact.

Jerry: Thanks, and then let’s address the last one in Chapter 12 – the alphabet soup statutes – the FDCPA. The statute governs debt collection practices, and while it doesn’t address credit reporting directly, it’s closely related, because debt collectors obviously rely upon credit reports when they pursue collection. The FDCPA regulates how they can communicate with individuals, the information they must disclose, and their conduct during the collection process. In essence, it’s a companion statute that protects consumers in the broader context of credit and debt. What were the notable trends under these statutes over the last 12 months?

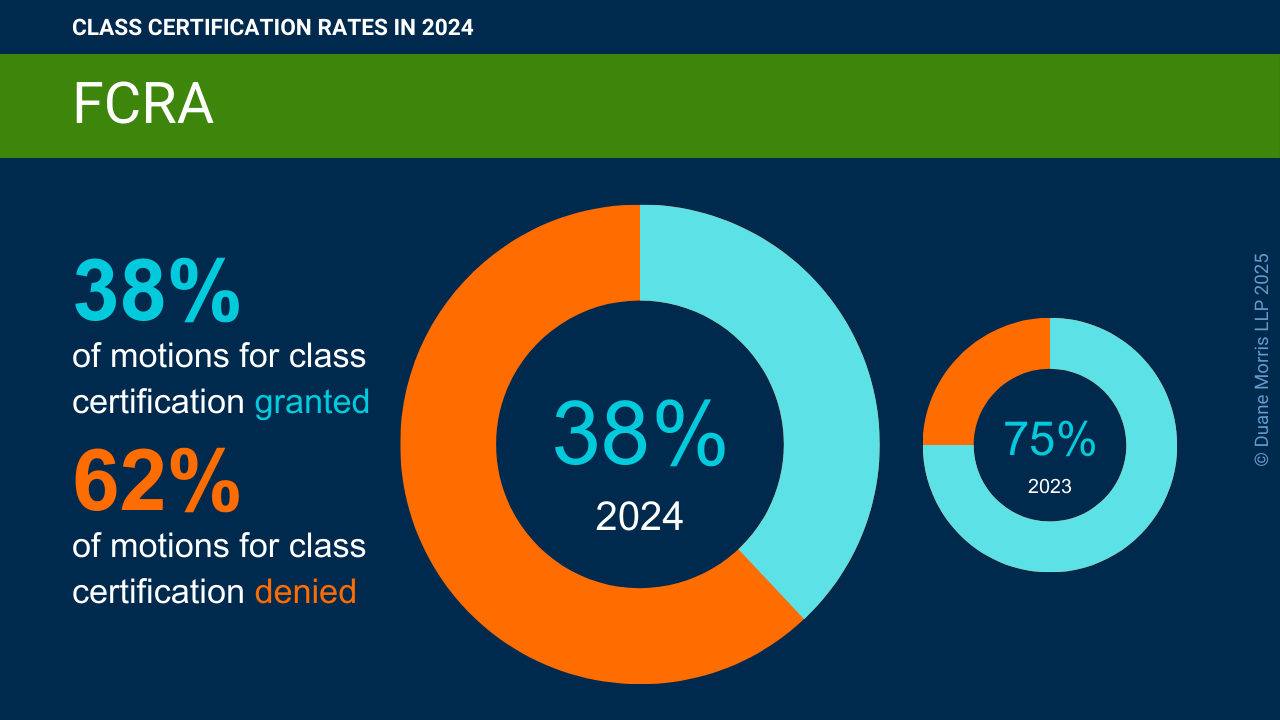

Shannon: One major trend we’ve seen in 2024 is a reduction in class certification success rates. Courts granted class certification in only 38% of FCRA, FACTA, and FDCPA cases, which is down from 75% in 2023. This could be partly due to the 2021 TransUnion decision and the increasing complexity of FCRA violations. Employers and consumer reporting agencies are now more careful about complying with technical requirements and plaintiffs are facing higher hurdles improving harm.

Shireen: Yeah, and another thing we’re seeing is the rise of state level laws that track the FCRA, but they impose even stricter standards. I’m sitting here in California – we definitely have some states like California, New York, and Texas, they have their own consumer credit reporting laws – and companies need to stay on top of both the federal and the state regulations to avoid potentially very significant liability.

Jerry: As our clients see in many spaces, there’s quite a patchwork quilt of laws and the legal environment is under constant change and flux. Were there important rulings in this space in 2024 that our listeners need to keep in mind?

Shannon: There certainly were. The Third Circuit issued a significant ruling in favor of the defendant in Barclift, et al. v. Keystone Credit Services, LLC. The defendant was a debt collector there, and engaged RevSpring, a third-party vendor, to print and mail debt collection notices to individuals, including the plaintiff. The plaintiff alleged defendant shared her personal information with RevSpring without her consent in violation of the FDCPA. The district court dismissed the plaintiff’s allegations without prejudice, ruling that she lacked standing because her alleged injuries were not sufficiently concrete, and thus she failed to allege a concrete injury under Article III standing requirements. On appeal, the Third Circuit affirmed the district court’s ruling. The Third Circuit determined that the plaintiff’s intangible harms must have a close relationship to alleged recognized harms for standing purposes, and the Third Circuit concluded that the plaintiff failed to establish standing because she could not show a close relationship between the harm she alleged, which was disclosure of personal information to the mailing vendor, and harms traditionally recognized by disclosure of personal information, including humiliation or embarrassment due to the public disclosure of sensitive information, and the Third Circuit opined that harm from internal disclosures such as that alleged by the plaintiff did not align with harms traditionally recognized in privacy torts that depend on public disclosure, unless there’s a sufficient likelihood of external dissemination.

Jerry: That’s a really interesting ruling, and certainly shows the range and kinds of information that are protected and what goes beyond just the mere scope of the information. Are there any other appellate rulings, Shireen, that you think our listeners ought to keep uppermost in mind for the coming year?

Shireen: Yeah, the Eleventh Circuit ruled on standing issues in Santos, et al. v.Healthcare Revenue Recovery Group, LLC. You know, these standing issues have been getting ironed out, up and down to the Supremes and back, quite a bit over the last 10 or so years. Here, the plaintiffs allege that the defendant provided inaccurate credit reports. The district court initially denied class certification, reasoning that consumers seeking statutory damages for willful FCRA violations needed to prove actual damages. The plaintiffs argued that they could recover statutory damages without proving actual damages and the case focused on interpreting 15 U.S.C. § 1681n(a)(1)(A), which allows consumers to seek statutory damages ranging from again $100 to $1,000 for willful violations. And on appeal, the Eleventh Circuit clarified that under statute, consumers do not need to prove actual damages to obtain statutory damages. The court noted that the statute distinguishes between the actual damages required under one provision and the damages available under the second, which does not require proof. So, the Eleventh Circuit’s interpretation aligned with decisions from other circuits, and furthermore, the court ruled that the district court’s denial of class certification was based on incorrect interpretation of the damages provision, and remanded the case for further proceedings. So, we’ll be keeping an eye on that as well.

Jerry: In terms of settlement dollars overall in 2024, how successful was the plaintiffs’ bar in monetizing their class claims.

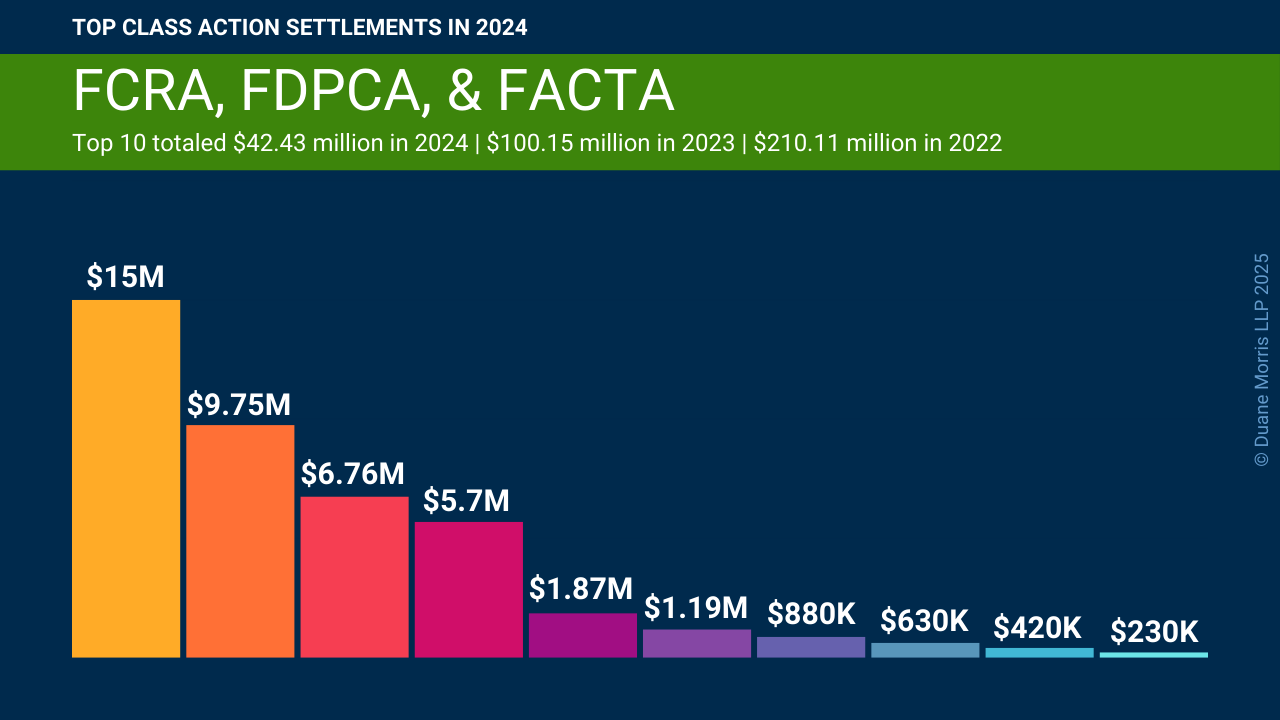

Shireen: So, there was actually a big drop in the numbers recovered in the top 10 cases in 2024 over 2023. In2024, the top 10 FCRA FACT Act, and FDCPA. Settlements totaled $42.43 million, and in 2023, that was a $100 million. So, more than double. Alittle bit surprising, but we’ll look to see what happens in 2025.

Jerry: Yeah, my prediction is in 2025 – my sense is those numbers are going to double, if not triple. and that’ll be an area that we’ll be tracking with interest in the Duane Morris Class Action Review for 2026. Well, thank you both for being here and for sharing your thought leadership with respect to class action litigation in this space. Listeners, please stop by our blog for a free copy of the FCRA Class Action Review e-book.

Shannon: Thanks so much for the opportunity, Jerry.

Shireen: Thanks, Jerry. Thanks, listeners.